Filed Pursuant to Rule 424(b)(4)

Registration Statement No. 333-251612

P R O S P E C T U S

9,600,000 Shares

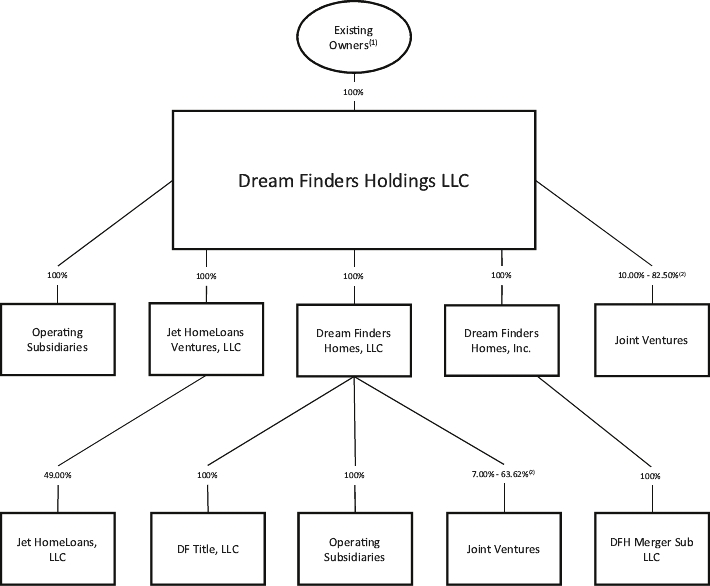

Dream Finders Homes, Inc.

Class A Common Stock

This is Dream Finders Homes, Inc.’s initial public offering. We are selling 9,600,000 shares of Class A common stock.

Prior to this offering, there has been no public market for our Class A common stock. We have been approved to list our Class A common stock on The Nasdaq Global Select Market (“Nasdaq”) under the symbol “DFH.”

Following this offering, we will have two classes of authorized common stock, Class A common stock and Class B common stock. The rights of the holders of Class A common stock and Class B common stock are identical, except with respect to voting, transfer and conversion. Each share of Class A common stock is entitled to one vote per share and is not convertible into any other shares of our capital stock. Each share of Class B common stock is entitled to three votes per share and is convertible into one share of Class A common stock. Outstanding shares of Class B common stock will represent approximately 85.4% of the voting power of our outstanding Class A common stock and Class B common stock immediately following this offering, assuming no exercise of the underwriters’ option to purchase additional shares of Class A common stock, with our directors, executive officers and principal stockholders representing approximately 94.4% of such voting power.

Immediately after this offering, we expect to be a “controlled company” within the meaning of the Nasdaq corporate governance standards. See “Management—Controlled Company Status” in this prospectus for additional information.

We are an “emerging growth company,” as that term is defined under federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. See “Prospectus Summary—Implications of Being an Emerging Growth Company” in this prospectus for additional information.

Investing in our Class A common stock involves a high degree of risk. See “Risk Factors” beginning on page 23 of this prospectus.

| | | Per Share | | | Total | |

Initial public offering price | | | $13.00 | | | $124,800,000 |

Underwriting discount and commissions(1) | | | $0.91 | | | $8,736,000 |

Proceeds, before expenses(1) | | | $12.09 | | | $116,064,000 |

(1) | The underwriters will also be reimbursed for certain expenses incurred in the offering. See “Underwriting” for additional information regarding underwriting compensation. |

The underwriters may also exercise their option to purchase up to an additional 1,440,000 shares of Class A common stock from us, at the initial public offering price, less the underwriting discount, for 30 days after the date of this prospectus.

Certain entities affiliated with BOC DFH, LLC, a holder of more than 5% of our Class A common stock and a wholly owned subsidiary of Boston Omaha Corporation (Nasdaq: BOMN), have agreed to purchase 2,385,000 shares of our Class A common stock in this offering at the initial public offering price. The underwriters will receive the same discount from any shares of Class A common stock sold to such entities as they will from any other shares of Class A common stock sold to the public in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares of Class A common stock are expected to be delivered on or about January 25, 2021.

BofA Securities | | | RBC Capital Markets | | | BTIG |

Builder Advisor Group, LLC | | | | | Zelman Partners LLC |

TCB Capital Markets | | | | | Wedbush Securities |

The date of this prospectus is January 20, 2021